Climate Safe COP26 Takeaways

By James Vaccaro, November 2021

Climate Safe Lending Network participants were engaged in a variety of ways, both in-person and virtually, during COP26 in Glasgow. For example, we have had a great reaction to The Good Transition Plan (which was presented at the Green Horizons Summit at COP26 and will be discussed at a webinar hosted by UNEP FI on 9th December). We also continue to be engaged in the Glasgow Financial Alliance for Net Zero (GFANZ) via the network’s role on the advisory panel.

We’ve had so many conversations with individuals across the network sharing their reflections – from minor triumphs to bruising disappointments; the expectations and emotions had never been higher. And finance had never been so firmly under the spotlight. That’s only likely to increase as the temperature rises (in every sense) on the road to COP27 in Egypt next year.

The Final Countdown, Until the Next One

The big headline of what was agreed at COP26 is that the governments have agreed to tighten what they came up with in their emission-reduction Nationally Determined Contributions (NDC) plans – which collectively added up to around 2.4 degrees Celsius of warming and will have another go next year to see if they can get closer to the 1.5oC target that COP26 attempted to keep alive. We heard the testimony of the catastrophic implications for vulnerable island states on the world going above 1.5-degrees. As previous head of the UNFCCC, Christiana Figueres, said: “No one in their right mind is talking about ‘well below 2°C’ anymore.”

Governments can react to changing conditions and it’s not impossible for them to keep ‘ratcheting up’ ambition; although the longer they leave converting this into action, the faster they would have to go, and those plans are already barely plausible. But if everyone has to go back and ‘have another go’ what does that mean for banks?

Can Banks Rachet Up?

On Finance Day at COP26 (3rd November) the major announcement was on the milestone achieved by GFANZ which includes the Net Zero Banking Alliance alongside other net zero alliances. It announced $130 trillion worth of financial institutions who have signed on to the net zero goals. Importantly, this included a clear call for each financial institution to “deliver their fair share of 50% emission reductions this decade” (e.g., to 2030). There were several announcements of targets and intermediate plans from institutions including Morgan Stanley, Standard Chartered, Amalgamated Bank, Triodos Bank , Banque Postale and BBVA (if you have one that we missed, please share it!)

Banks setting out their plans now and over the course of the next 12 months might reflect on how feasible it would be to change or to ‘ratchet up’ their ambition once their plans are set. Arguably the loans that they make in the next 12 months are likely to be around in the economy for the next couple of decades, so they had better get those as close to a ‘right the first time’ from the perspective of aligning with 1.5 degrees. That’s why The Good Transition Plan suggested anchoring the highest ambition in the planning process. To deliver a fair-share of 50% by 2030 banks need to consider how relatively over-weight or under-weight they are in high-carbon assets. For any who are planning to reduce by less than 50%, they would need to explain why others would need to compensate.

We Need to Talk About Fossils

Many NGOs have pointed to the flows of finance from banks to the most damaging activities – such as to the expansion or extraction of fossil fuels (deemed by the IEA net zero scenario as being incompatible with 1.5-degrees) – needing to be the focus for banks in the near term. And it is those finance flows which were not mandatory for banks in their net zero pledges. Many argue that these flows are implicitly ‘not possible’ with a 1.5-degree world, but some banks to continue to say that fossil fuel investments will continue despite net zero pledges.

There was, notably, a single mention of fossil fuels in the final COP26 document agreed by governments. Only one, and surprisingly the first mention of fossil fuels in the final agreed document at a COP. One might have thought that in the previous 25 attempts, someone might have thought to include fossil fuels, not least since they are the biggest contributor towards climate change (and we’ve known about that for decades). But in building a global consensus, it is not easy to move beyond the pace of the slowest. So creative language is often introduced to create sufficient room for interpretation – leaving a window open to do better (albeit with the door open to continue as before in the meantime).

The final pact – see full text – includes a passage to accelerate ‘efforts towards the phasedown of unabated coal power and phase-out of inefficient fossil fuel subsidies, while providing targeted support to the poorest and most vulnerable in line with national circumstances and recognizing the need for support towards a just transition.’

War of the Words

The two most controversial phrases from the final Cop26 agreement were:

- ‘Phasedown of unabated coal’ (Why not phase-out, and is fully-abated coal really a plausible economic concept?); and

- The ‘phase out of inefficient fossil-fuel subsidies’ (Granted, those subsidies can come in a variety of forms and are often indirect. But without defining what efficiency would be or who they would be inefficient for, makes this a troublesome phrase. Those subsidies are pretty efficient for fossil fuel companies and those financing them right now)

It's worth noting that the wording from the GFANZ Call to Action was much stronger – calling for phase-out goals for fossil fuels and fossil fuel subsidies. The irony on the wording for coal is that in countries who argued hardest for this compromised wording – like India – are themselves likely to be facing challenges due to the economics of energy. India’s energy sector is transforming rapidly due to the expansion of renewable energy with solar energy now undercutting existing prices where coal can continue to run profitably. That has led to fossil fuel subsidies to try and prop up the coal sector (certainly inefficient for a just transition as they charge more to Indian consumers to continue with a polluting energy source) and ultimately it is unlikely to work since there are still likely to be stranded assets and bank debt that won’t get repaid. Solar also provides considerably more jobs than coal.

The positive elements of COP26 included an agreement on an end to deforestation by 2030. And this is something that needs to be reflected in the details monitored and enforced by banks. The same pledge was also made 7 years ago, but since then (2014-2021) deforestation has still continued. In some regions, forests have disappeared faster than before and some fear that the underlying conditions haven’t changed. Some banks have been accused of not following through on their own promises regarding deforestation, which suggests that a regulatory approach may be necessary (perhaps via an extension of the One-for-One proposal for new fossil fuels to apply to deforestation).

Digging Deeper

What will certainly be required for progress on this (or agreements on methane reductions) is for banks to get a better understanding of their supply chains and the impact of their finance. As we set out in The Good Transition Plan the concept of enhanced due diligence and KYCO2 (know your carbon) should apply to knowing your deforestation or methane or biodiversity footprint. There are now methodologies available (subject to consultation via the Partnership for Carbon Accounting Financials (PCAF) running until 17 December 2021) including accounting for carbon emissions removals and capital market instruments, so ‘lack of methods’ is no longer a barrier. And the Science Based Targets Initiative (SBTI) are updating their methodology to validate net zero targets for banks commensurate with a 1.5-degree pathway - again subject to a consultation process that is now open.

Banks and Bankability

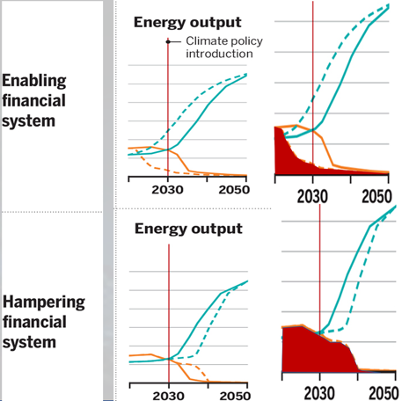

The role of financial institutions is pivotal in either speeding up or slowing down the Nationally Determined Contributions (NDCs). In a paper recently published in Science, the pathway of coal and renewable energy were modelled without the simplifying assumption that ‘finance is neutral’. The results demonstrate a very significant difference to the pace of change – and the all-important ‘area under the curve’ (cumulative emissions – added by CSLN) is less than half in an enabling financial system that speeds up the transition.

Accounting for finance is key for climate mitigation pathways (Battiston, Monasterolo et al, 2021)

In 2022, Climate Safe Lending Network will be exploring the concept of how financial institutions can be enabling and lead the way in accelerating climate solutions. A lot will hinge on transforming some key mindsets, such as whether the notion of ‘bankability’ is a fixed constant. Or if it’s a function of a bank’s abilities and their understanding and perception of risk which can be transformed by more focused attention and deeper relationships with clients. If banks see themselves as neutral, do they become neutral? And if they were to see themselves as leaders, would they become leaders? Banks might need governments to put the right policies in place to drive climate solution markets. The deep retrofit of buildings, the decarbonization of transport, and the growth of green hydrogen and its use in manufacturing processes, will need to surge forward – even faster than the growth of renewable energy. But banks need not be passively waiting for policy; they can play a proactive role in co-creating the optimum interventions to drive innovation and progress together with their clients, unpacking the risks and identifying the leverage points to grow new markets.

Capital for Causes and Consequences

Beyond voluntary actions led by private sector organisations and banks, it is generally regarded that regulatory interventions are most likely to drive change across the sector and the economy.

The UK Chancellor set out plans to make transition plans mandatory by 2023. The Bank of England has set out its plans to green its monetary policy – changing the criteria for bond purchases based on supporting the transition to net zero. But it appears to be sticking to a capital requirements framework that only addresses the consequences and not the causes of climate change. This leaves those responsible for contributing the most to climate change with no intervention. It’s not clear how that part of the Bank’s policy is incorporating net zero into its policy; however, it is likely to debated further in 2022.

As reported in POLITICO’s Morning Money on 16th November, the Basel Committee on Banking Supervision (BCBS), released a statement earlier this month that it will consult on “a set of principles for the effective management and supervision of climate-related financial risks at internationally active banks” which involves assessing and potentially developing measures for disclosure, supervision and regulation. This announcement could lead to capital surcharges, particularly since EU and UK central banks are calling upon “lenders to identify which parts of their balance sheet are exposed to climate change.” Frank Elderson, vice chair of the European Central Bank’s Supervisory Board, noted according to POLITICO that a risk-based approach would eventually lead to banks setting aside more capital “because capital is there to be set against material risks and these are material risks.”

There are new ideas being put forward in different corners of the world - like this one in New Zealand, which proposes a mechanism to own and manage legacy high-carbon assets to accelerate the phase out of fossil fuels in the optimal way. We will bring these ideas and examples into discussions within the network on a climate transition resolution fund (i.e., Bad Bank).

The Path Ahead

There's a line in Rebecca Solnit's book, Hope in the Dark: "Most victories will be temporary, or incomplete, or compromised in some way, and we might as well celebrate them as well as the stunning victories that come from time to time. Without stopping."

Amidst the disappointment that the global agreement was not all it could have been including no progress on a firm international carbon floor price or other elements, there were many small victories and useful contributions that can be celebrated. There are useful developments which didn’t get the spotlight but are likely to be useful – not least the GFANZ net zero financing roadmap.

*****